Setting up a business in India is a dream for many entrepreneurs and startup founders. But while launching your Private Limited Company may feel like a major milestone, it’s just the beginning. One of the most critical yet often overlooked aspects of running a business in India is company compliance.

From maintaining books of accounts to filing annual returns, compliance is not just a legal requirement but a strategic necessity. Ignoring it can lead to penalties, reputational damage, and even closure of your business.

This guide is your go-to resource to understand compliance for Private Limited Companies in India. We’ll break it down in simple terms and provide actionable steps so you stay ahead and stay compliant.

What Exactly is 'Company Compliance' in India?

Company compliance refers to following the laws, rules, and regulations prescribed under the Companies Act, Income Tax Act, GST Act, and labour laws. It ensures your business is operating legally and ethically.

The major governing bodies include:

- Ministry of Corporate Affairs (MCA) – for ROC filings & company law.

- Income Tax Department – for tax returns & TDS compliance.

- GST Council – for GST registration and return filings.

Why is Compliance Crucial for Your Private Limited Company?

- Legal Standing: Timely compliance protects your business from penalties, fines, or even disqualification of directors.

- Credibility & Trust: A compliant company attracts customers, investors, banks, and vendors by building confidence.

- Smooth Operations: Avoid operational roadblocks or legal interruptions that may arise from non-compliance.

- Access to Funding: Investors and financial institutions prefer companies with a clean compliance record.

Key Compliance Requirements for Private Limited Companies in India

1. Ministry of Corporate Affairs (MCA) / ROC Compliance

- Annual Filings:

- Form MGT-7: Annual Return with company details.

- Form AOC-4: Financial statements including profit & loss and balance sheet.

- Board Meetings: At least 4 board meetings per year with minimum gap requirements and proper minutes.

- Annual General Meeting (AGM): Must be held within 6 months from the end of the financial year.

- Maintain Statutory Registers: Registers for shares, members, directors, etc., must be maintained.

- Director KYC: Every director must file DIR-3 KYC annually.

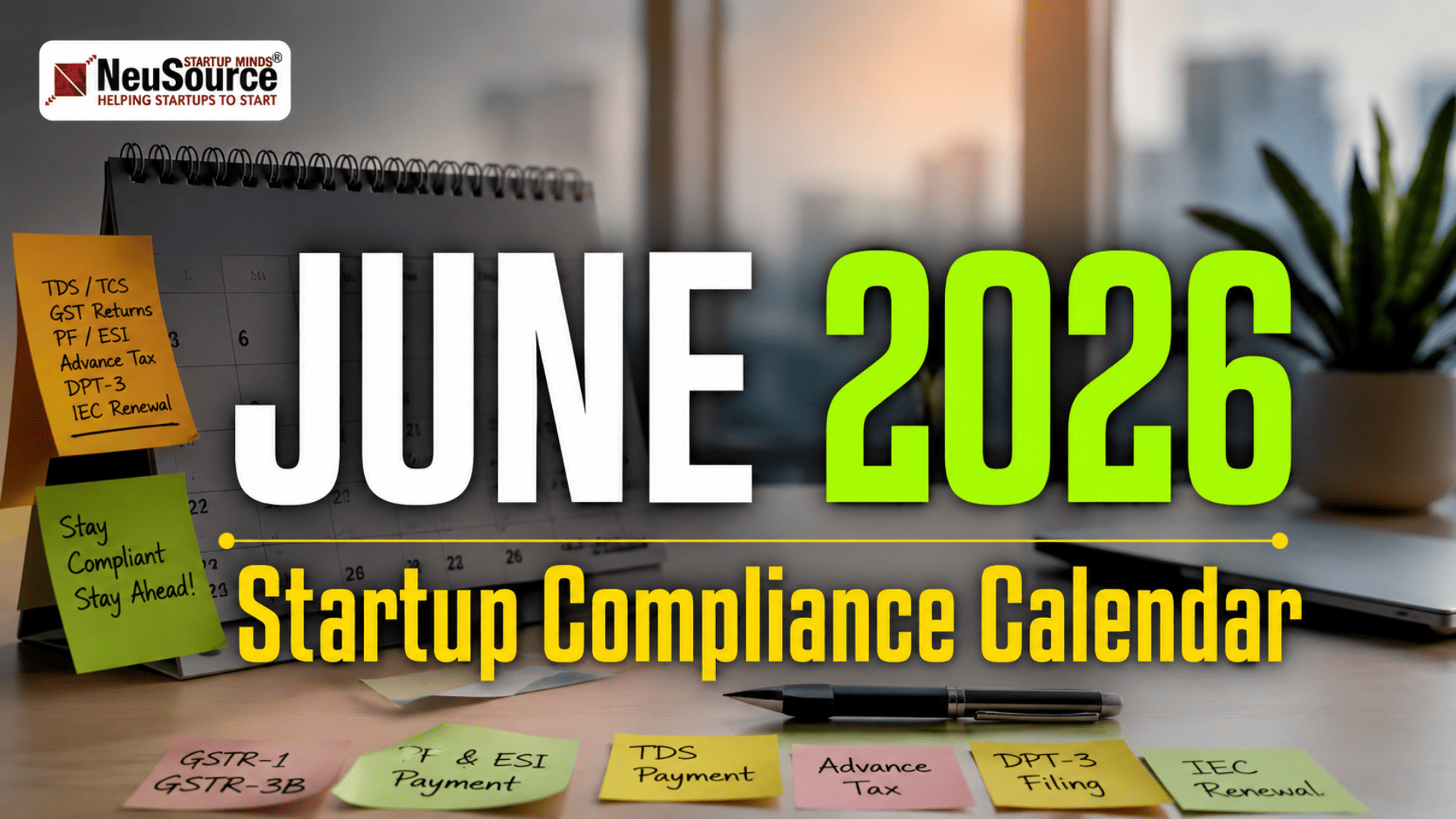

2. Income Tax Compliance

- ITR Filing: Income Tax Return must be filed annually by the company.

- TDS Compliance:

- Deduct TDS on payments like salary, contractor fees, rent, etc.

- Deposit TDS with the government on time.

- File quarterly TDS returns (Form 24Q, 26Q).

- PAN & TAN: Mandatory for tax-related activities and TDS compliance.

3. Goods & Services Tax (GST) Compliance

- GST Registration: Mandatory if turnover exceeds threshold limit or based on business type.

- GST Return Filing:

- GSTR-1: Monthly/Quarterly outward supply return.

- GSTR-3B: Summary return of sales, purchases, and tax paid.

- E-Invoicing: Mandatory for companies with turnover above prescribed limits.

4. Other Important Compliances

- Professional Tax: Applicable in certain states.

- PF & ESI: Compulsory if employee count crosses thresholds.

- Labour Law Compliance: Including minimum wages, gratuity, maternity benefits, etc.

- Audit Requirements: Statutory audit mandatory for every Pvt Ltd company.

Penalties for Non-Compliance: Don’t Get Caught Off Guard!

Ignoring Private Limited Company compliance can have serious consequences:

- Late filing penalties up to ₹100 per day per form.

- Disqualification of directors under Section 164 of the Companies Act.

- Heavy fines for TDS/GST defaults.

- Freezing of bank accounts or even company strike-off.

It’s always better to invest in compliance rather than pay the price of negligence.

Tips for Ensuring Smooth Compliance for Your Pvt Ltd Company

- Maintain Records: Keep books of accounts, invoices, and meeting minutes up to date.

- Stay Updated: Keep track of changes in Company Law India, taxation, and GST rules.

- Hire Professionals: Engage a qualified CA, CS, or legal firm to handle your startup compliance in India.

- Set Reminders: Create a compliance calendar for key due dates.

- Use Digital Tools: Invest in compliance management software to automate filings and alerts.

Conclusion: Your Path to a Compliant & Thriving Business

Compliance is not just about meeting legal requirements—it's about building a sustainable and credible business. For any Private Limited Company in India, staying compliant unlocks long-term growth, funding opportunities, and peace of mind.

Think of it as an investment, not an expense. A little attention today can save you from massive trouble tomorrow.

Need help with your company’s compliance? Contact our experts today and stay legally strong and financially safe!

Janki Gupta

The internet offers opportunity, but only strategy builds success. Don't just exist online—dominate. Choose Neusource to craft your digital footprint and lead your business to its peak.