NOTICES ISSUED UNDER SECTION 142(1) TAX NOTICE?

Income tax notices are a very loosely defined term in India. The taxpayers get scared without understanding the type of income tax notice and reason/s for the same. In this article, we will discuss the various type of IT Notice issued by the Income Tax Department

Income tax notices are a very loosely defined term in India. The taxpayers get scared without understanding the type of income tax notice and reason/s for the same. In this article, we will discuss the various type of IT Notice issued by the Income Tax Department

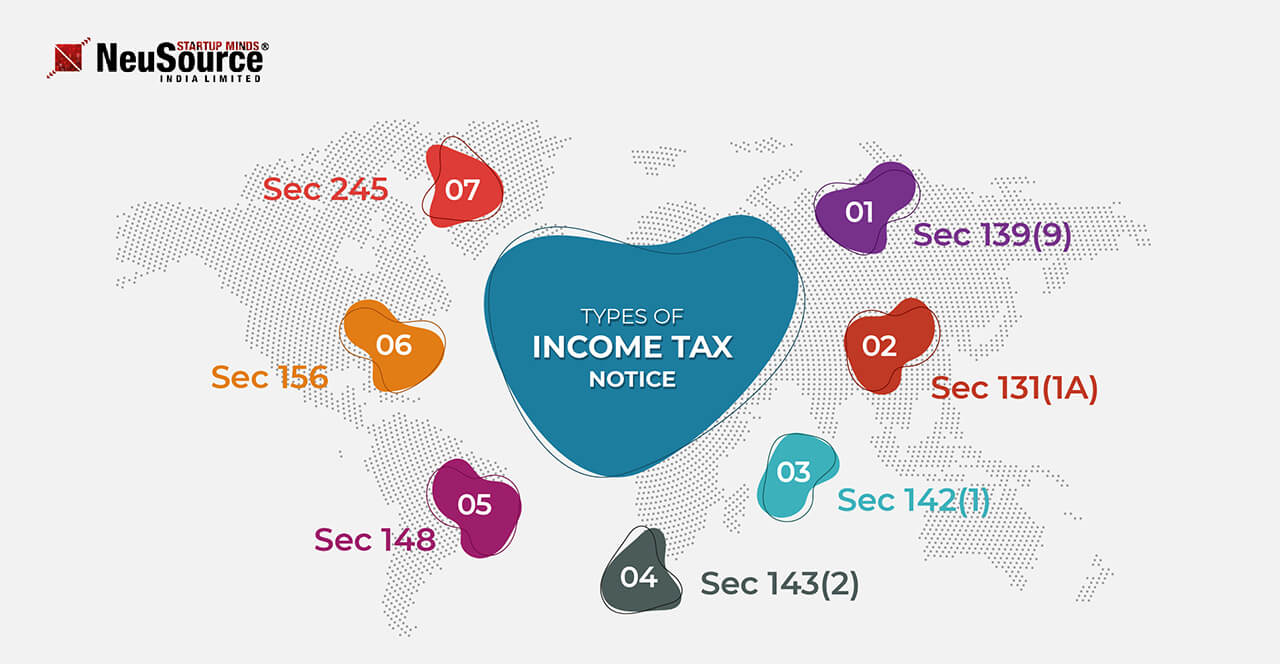

- Sec 139(9): Defective Income Tax Return, In this case, the Assessing Officer gives an opinion that ITR documented by the assessee is deficient. Best of all, an appropriate mistake depiction is shared and the Assessing Officer additionally recommends a plausible answer for redress the equivalent. The assessee is allowed a chance to react inside 15 days from the date of suggestion or before it is surveyed. On the off chance that you don't react inside 15 days, at that point your arrival will be dismissed by the AO. The imperfection u/s 139(9) can be an inappropriate ITR recorded, missing data, and deficient return, etc. You may concur or differ with the perception of the Assessing Officer. In most of the cases, without going into the benefits, the assessee acknowledges the deficiency. This is one of the basic errors by the assessee. On the off chance that you don't agree with the error/defect, at that point you can answer to the Income Tax Department. The main catch is you should know all the standards.

- Sec 131(1A): Undisclosed/Concealed Income If you AO thing that or having an opinion that you are hiding the income or likely to hide income then you will receive income tax notice u/s 131(1A). This notice is an intimation that AO is giving a right to investigates the team into that matter. The assessing officer can seize the books of account or other documents by providing reasons for the same. There is NO particular time limit to serve this notice.

sec 142 1 of income tax act

- Sec 142(1): Preliminary Enquiry before an assessment You will get a notice of preliminary inquiry in case the return has not filed on time. Alternatively, if the Assessing Officer would like to go through the documentary proof to verify your claim in IT Return then he may ask you to show the related documents for assessment. As far as possible to serve the notice u/s 142(1) is before the end of the relevant assessment year. For example, the income tax return filed for Assessment Year 2016-17, you can get notice u/s 142(1) on or before 31st March 2017. The limit is not valid in case the return is not filed by the assesses.

- Sec 143(2): Follow up to the notice u/s 142(1) Due to any reason Assessing Officer is not satisfied with the response provided by the assesses or not able to provide the documents against notice u/s 142(1) as clarified in the point for Sec 142(1) then you will receive notice u/s 143(2). Under this scenario, the case is called for detailed scrutiny. The AO may ask the assesses to either manage his office in person or produce supporting, particulars and evidence in support of his claim. There is a time limit under which notice may be served u/s 143(2) is within six months from the end of FY in which the return is furnished. For example, the return for FY 2016-17 was filed in FY 2017-18 on or before 5th Aug 2017. The end of FY 2017-18 is 31st Mar 2018. Six months from the end of FY 2017-18 is 30th Sep 2018. Therefore, notice can be served until 30th Sep 2018.

- Sec 148: Income escaped assessment If your new Assessing Officer does not agree with the assessment of previous Assessing Officer then you can expect notice u/s 148. In short, even after assessment, if the Assessing Officer believes that some income of the assesses escaped assessment then income tax notice u/s 148 can be issued. Assesses may be asked to file the income tax return for the relevant assessment year from the end of the relevant assessment year notice may be served within 4 years and if the income escaped assessment is Rs 1lakh or less than that. Otherwise, the notice served by the department within 6 years from the end of the relevant assessment year. For example, for a return filed in AY 2017-18, an income tax notice can be served on or before 31st March 2022 (for 1lakh or less than 1lakh cases). In the case of more than 1lakh cases, the income tax department may serve notice till 31st March 2025.

- Sec 156: Notice may be served for Pending Demand If any amount like a penalty, interest, etc need to be pay by the taxpayer to the income tax notice may be served by IT Department u/s 156. Normally the department is served this notice after the assessment of ITR. The taxpayer can deposit the amount to be paid within thirty days from the date of the income tax notice. There is no time limit to serve this notice. Income tax notice under section 143(1) and 200A are also considered as Notice of Demand.

- Sec 245: Refund adjusted against the tax demand It is an intimation from the Income Tax department. This notice is issued if their tax refund (full/partial) for a relevant assessment year and the same has been adjusted against the tax demand due to the taxpayer. There is no time limit to serve or send income tax notice/intimation u/s 245. Normally taxpayers get confused between Notices and Intimation received from the Income Tax department. The 4 major assessments under income Tax law is Intimation U/s 143(1), 143(3), 144 or 147 these are not noticed from the department side.

Neusource Startup Minds is the Best Business management consultant in Delhi, Offer various services like Proprietorship Firm Registration, OPC Registration, LLP Registration. Neusource Startup Minds provides a wealth of proficiency and best practices in tax administration and process expansion for effectively managing the GST compliance Process, Compliance Package for Pvt Ltd Company, OPC Compliances Packages.

Lalita Sharma

"Ideas are easy but Implementation is Hard”. Neusource is the platform for making a right choice in every aspect of business that helps to grow your business and give assistance in each vital advance which causes your beginning up to create in each most ideal manner